Buying for the first time?

For first time buyers, getting onto the property ladder may seem like a daunting process, but there is help available.

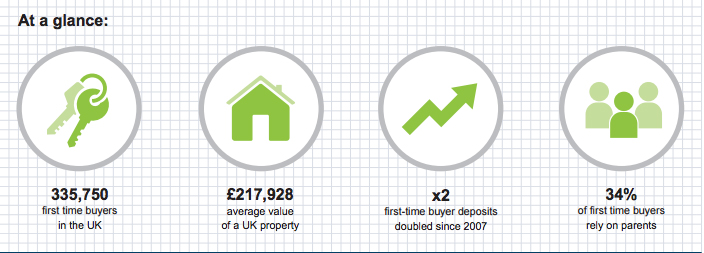

With demand outstripping supply in many areas, the average UK house price has been pushed beyond the reach of many of the UK’s estimated 335,750 first time buyers. A report from The Land Registry (based on data from November 2016) shows an annual price increase of 6.7%, taking the value of the average UK property to £217,928.

When you consider that first-time buyers would typically put down around 20% against their first home, it’s no wonder that finding a sufficient deposit is becoming increasingly difficult – especially for those currently renting. In fact, one of the major lenders reported the average first-time deposit has more than doubled since 2007 to more than £32,000.

If you’re struggling to save a large deposit you may be able to find a mortgage rate of 90% or 95% – provided you can meet the lender’s affordability criteria.

The bank of mum and dad

Meanwhile research by the Social Mobility Commission has found an increasing proportion are turning to their parents for help buying their first home. In fact, over a third of first-time buyers in England (34%) are relying on the bank of mum and dad, compared to one in five in 2010. The ‘bank of mum and dad’ has been a useful financial foot-up for many, but what about parents who want to help their kids but don’t have savings?

Government help

Although the Help to Buy: mortgage guarantee scheme ended in December 2016 the Help to Buy: Equity Loan is still available. The Government lends you up to 20% of the cost of your newly-built home, so you’ll only need a 5% cash deposit and a 75% mortgage to make up the rest. Equity loans are available to first time buyers as well as homeowners looking to move. The home you want to buy must be newly built with a maximum price tag of £600,000.

Other initiatives to help first-time buyers include The Help to Buy: ISA which helps you boost your savings by 25%. For every £200 you save you receive a government bonus of £50. The maximum government bonus you can receive is £3,000.

Sound mortgage advice can take the complexities out of the home-buying process and maximise your chances of getting an affordable mortgage.

Your home may be repossessed if you do not keep up repayments on your mortgage.